Stablecoins

What are stablecoins and why they are relevant?

Stablecoins are digital currencies on the blockchain whose price is pegged to a fiat currency, such as the US dollar – but the underlying collateral structures can vary widely. The most obvious benefit of stablecoins is their use as a medium of exchange, bridging the gap between fiat and cryptocurrencies. They can, however, offer an entirely different benefit over traditional cryptocurrencies: reducing price volatility.

As the name suggests, they aim to be price stable. This makes them a good store of value and encourages their adoption for day-to-day transactions. Furthermore, stablecoins increase the mobility of crypto assets within the ecosystem. Solana Pay is an early project supporting their use for everyday transactions. It collaborates with Circle, the issuer of USDC, and offers low cost, instant settlements to merchants.

Stablecoins open the door for existing financial markets to integrate with the rapidly growing decentralized finance (DeFi) industry. As a driver of market stability, they could act as the main vehicle for cryptocurrency adoption in loan and credit markets, potentially inheriting many of the functions formerly reserved for fiat money.

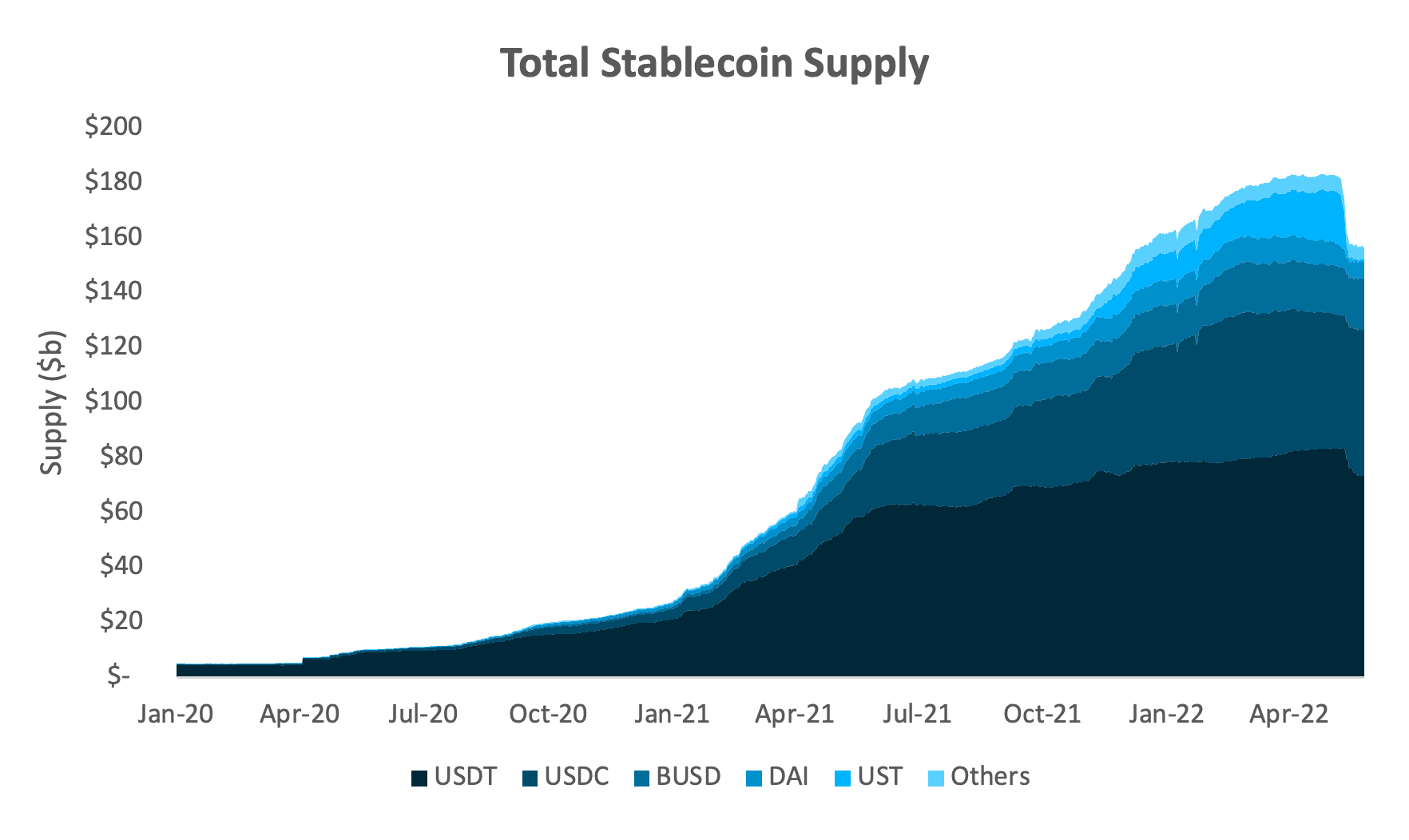

Given the growth of DeFi in 2020 and 2021, stablecoins gained prominence as they were deployed and demanded in many associated protocols. The total supply of stablecoins grew from $5.9bn in early 2020 to $155bn today.

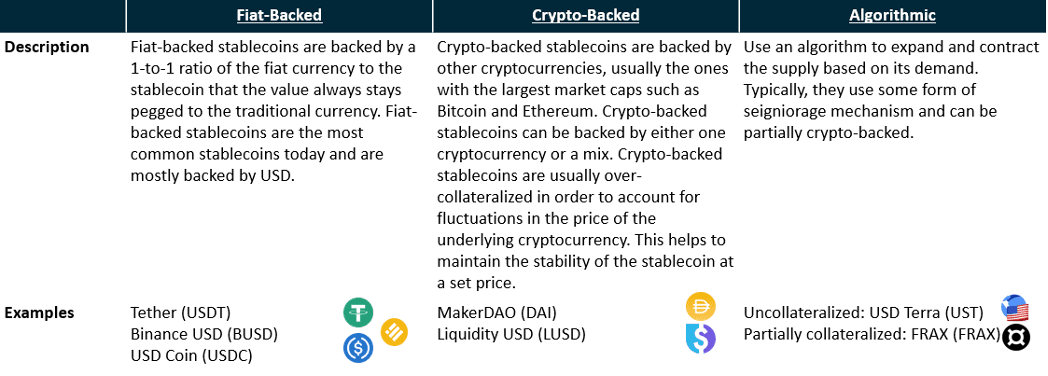

Three primary categories of stablecoin

Stablecoins can be grouped into three types, according to the mechanisms for maintaining the price peg. The most common mechanisms are:

Source: Own illustration

MakerDAO deep dive

Founded in 2014, MakerDAO is the issuer of the DAI stablecoin. Although the largest crypto-backed stablecoin, its market share is only about 4%. The main collateral used for minting DAI today is ETH, USDC and BTC.

Price stability is achieved through multiple mechanisms:

- Overcollateralization: To mint 1 DAI, users must deposit assets worth more than 1 USD. As of May 2022, the average collateralization ratio was 170% (Source: Link). This means that, on average, every 100 DAI are backed by assets worth $170. If the collateralization ratio falls below a predefined threshold, in this case 150%, the position is liquidated. By liquidating the position, MakerDAO does not take on any bad debt.

- Arbitrage: USDC can be used to mint DAI for free through the Price Stability Module (PSM). When DAI is above $1.00, arbitrageurs can make an immediate profit by taking 1 USDC, exchanging it for 1 DAI at MakerDAO, and selling it for a profit. Conversely, when DAI is below $1.00, arbitrageurs can buy 1 DAI at $0.99 and exchange it for 1 USDC (worth $1).

During the March 2020 downturn in capital and crypto markets, the MakerDAO system came to the verge of an emergency shutdown. A downward price trend turned into an outright collapse that unfolded over 36 hours between 12-13 March – it saw Ethereum down as much as -70% in a day at one point, and it closed down -55%. It meant numerous positions had to be liquidated, not only at MakerDAO, but across the entire Ethereum network and central exchanges. Due to the scale of auctions triggered, some of them were won by bidding just decimal points above zero. MakerDAO avoided an emergency closure and ensured all users (both Dai and Vault holders) received the net value of assets they were entitled to. Read more about the collapse. After the event, single-collateral DAI went obsolete and multi-collateral DAI was introduced. Currently, 45% of DAI's collateral consists of USDC, which significantly reduces the risk of de-pegging in the event of a severe sell-off. Mind you, Circle, the issuer of USDC, is a US-based company, which means the improvement comes at the price of centralization risk.

MakerDAO is also a pioneer in combining decentralized finance with traditional finance by providing loans to companies – such as a $20m loan to Société Générale and $75m via Centrifuge, a DeFi protocol that enables crypto-liquidity for off-chain assets.

MakerDAO is managed through its governance token MKR. While Maker is structured as a DAO, the funds raised during the seed phase were used to bootstrap the project. MakerDAO’s cumulative revenue for 2021 is estimated at $88m (Source: Link).

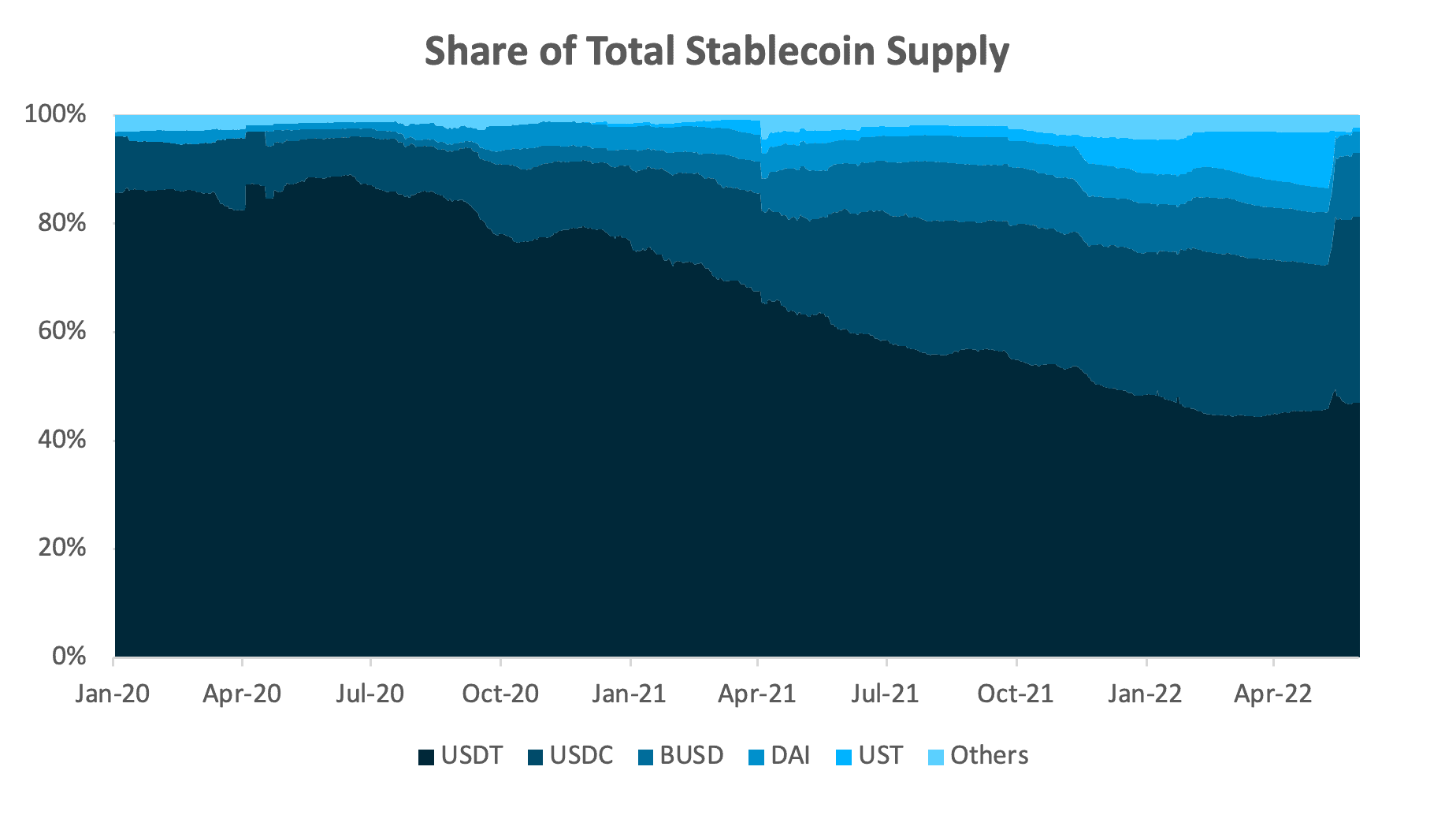

Stablecoin market dominance

Currently, fiat-backed stablecoins dominate the market. Despite accusations against USDT, stoked by a lack of transparency, that its reserves don’t contain the required assets, it still holds nearly 50% of the total stablecoin supply. In the UST aftermath, $10bn out of $83bn USDT have been redeemed. USDC follows at 34%, and then BUSD at 12%. UST was the 4th largest stablecoin just before its collapse.Stablecoins pegged to a fiat other than the U.S. dollar hold a mere 0.70% market share. Reasons for this low penetration include the dollarization of the economy, exchanges only dealing in coins pegged to USD, and negative interest rates on fiat reserves, making it difficult for issuers to make a profit.

Source: own illustration with date from Coingecko.com

Source: own illustration with date from Coingecko.com

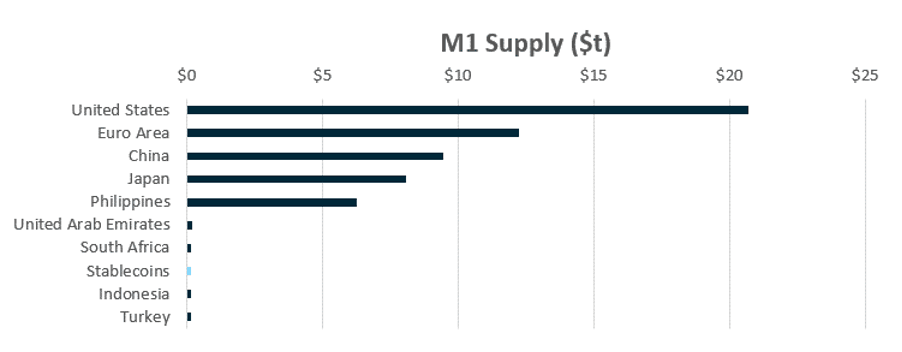

For perspective on the overall value of stablecoins, consider that the narrow measure of global money supply (‘M1’) is roughly $83,517bn (Source: Link). Narrow money is defined as all physical money such as coins and currency, demand deposits, and other liquid assets held by central banks. If stablecoins were added, they would account for approximately 0.20% of narrow money – their total supply size is comparable to countries such as South Africa, Indonesia, or Turkey.

Source: own illustration with data from Take-Profit.org

Hedging the stablecoin de-peg risk

Below we outline the three main strategies for hedging stablecoin de-peg risk, exploring their usefulness based on the recent UST de-peg.

- Short a perpetual future:

FTX is one of the only exchanges offering perpetual futures on stablecoins, providing them on USDT and UST. By shorting a perpetual future, the potential losses due to a price fall are covered by the profits from the short position. The cost depends on the funding rate, which fluctuates continuously over time and is difficult to predict given it’s driven by supply and demand. FTX listed the UST perpetual future on 28 January 2022. The average cost between the listing and the UST de-peg was around 10% per annum. The margin requirement is between 5-10%, which doesn’t earn interest and so incurs additional opportunity cost at the portfolio level. - Borrow against a fully collateralized stablecoin:

Deposit a fully fiat-collateralized stablecoin, such as USDC, on a (usually decentralized) exchange, and borrow the desired stablecoin against it. Only the number of coins needs to be returned, not the original borrowed value, thus creating a risk-neutral position for the borrowed stablecoin. The Anchor protocol on the Terra Blockchain, the native Blockchain of UST, paid up to 19.5% interest on UST, creating a high demand for it. Hence few investors provided UST to lending/borrowing protocols – combined with strong UST demand, the amount of UST available to borrow was therefore low. Plus, due to dynamic pricing, each additional borrowed UST increased the borrowing cost, leaving investors paying an interest rate over 10% and only enough liquidity for retail investors. Most lending/borrowing protocols have a maximum loan to value ratio of around 85% if USDC is provided as collateral, leaving a high capital inefficiency. - Insurance:

In recent years, decentralized insurance protocols have been introduced, some of which cover stablecoin de-pegs – albeit for a very limited selection of coins. On UST, the largest non-fiat backed stablecoin, insurance policies were offered by five different protocols. The two largest providers were Nexus Mutual, with $82m in coverages, and InsurAce, with $22m. Out of the total UST, which peaked at $18.7bn, the total insured value was between 0.5-1%. The insured amount was limited mostly by the insurance protocols, because there was insufficient liquidity for additional policies. Of the five protocols, only InsurAce and Unslashed Finance paid out the coverage. InsurAce paid only $11.7m of the $22m insured, due to eligibility criteria that need to be cumulatively fulfilled. Unslashed Finance has paid out 1,000 ETH ($1.9m) up until now. Nexus Mutual stated it only insured the protocol risk of Anchor, not any de-peg risk of UST, and is not therefore paying out on the latter.

In summary, there are several strategies to hedge the de-peg risk of stablecoins, but their availability is limited – and where they are available, the costs often outweigh the benefit of achieving risk-neutral returns.